Concealed Carry Insurance

Do You Really Need CCW Insurance?

The concealed carry community faces a tough question: is CCW insurance worth the monthly premium? Legal defense costs from self-defense incidents can reach six figures, potentially destroying your financial future.

At Cloudster Pillow, we believe every responsible carrier should understand the real financial risks they face. The decision isn’t just about monthly payments-it’s about protecting everything you’ve worked to build.

What Concealed Carry Insurance Actually Covers

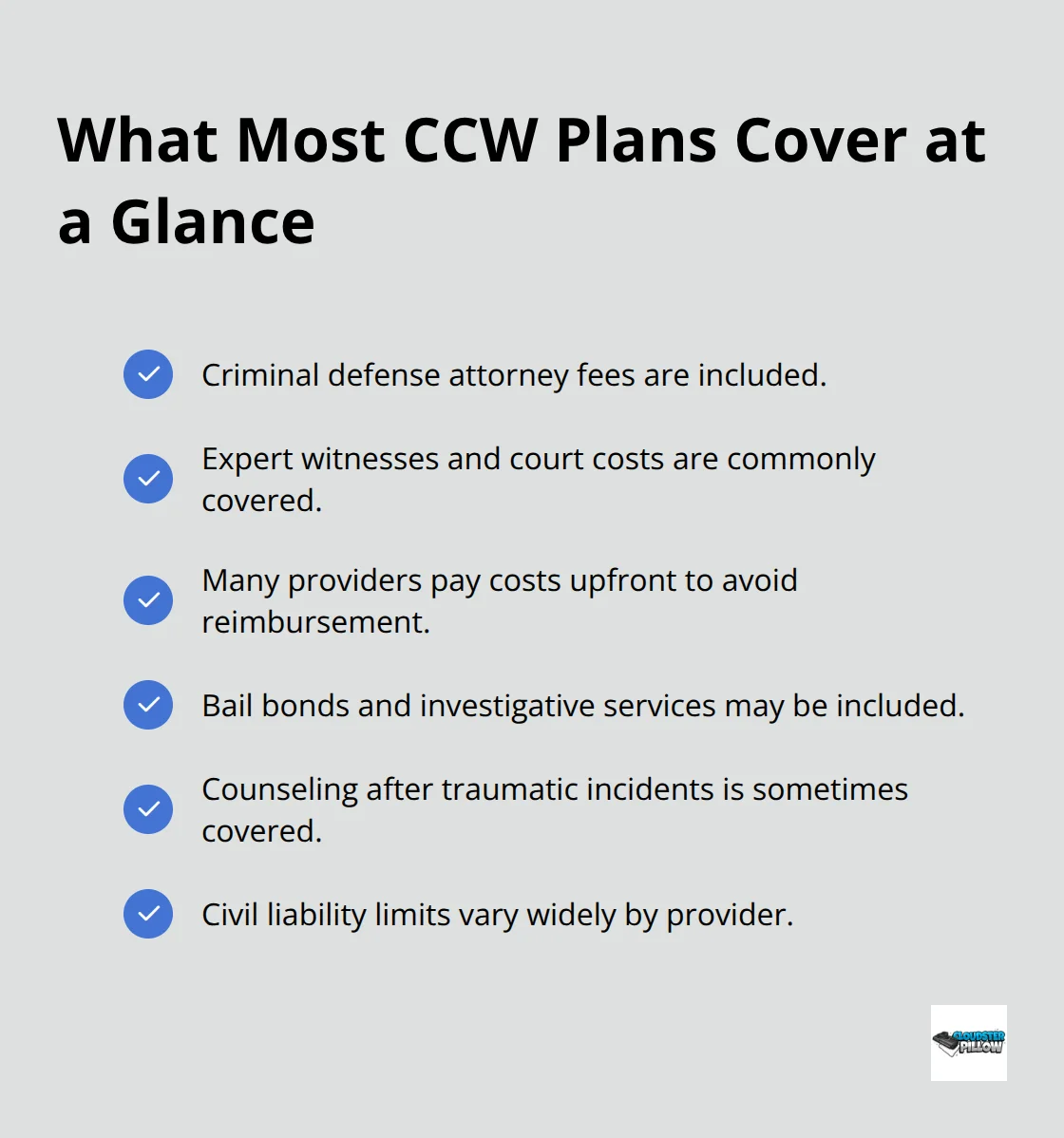

Concealed carry insurance functions more like a legal defense membership than traditional insurance. These plans cover specific costs when you face legal action after a self-defense incident. Most providers cover criminal defense attorney fees, with companies like CCW Safe providing unlimited legal defense coverage while others cap expenses at $100,000 to $250,000.

Attorney fees range from $100 to $500 per hour, making unlimited coverage a smart financial decision. Civil liability protection varies dramatically between providers-USCCA offers up to $2 million for civil cases, while some budget options provide minimal or zero civil coverage.

Legal Defense Cost Structure

Criminal defense coverage handles your attorney fees, expert witnesses, and court costs when prosecutors charge you with a crime. Most quality providers pay these costs upfront rather than requiring reimbursement (which protects you from immediate financial strain). Some plans also cover bail bonds, investigative services, and psychological counseling after traumatic incidents.

Civil liability coverage protects against damages awarded to plaintiffs who sue you for medical bills, lost wages, or wrongful death claims. These cases proceed independently from criminal proceedings and often result in substantial financial judgments even when criminal courts find your actions justified.

Criminal Cases vs Civil Lawsuits

Criminal cases focus on whether you broke the law, while civil cases determine if you owe money to the person you shot or their family. Studies show 1.82 million defensive gun uses occur yearly, with many facing subsequent legal challenges. Many carriers wrongly assume criminal acquittal prevents civil lawsuits-this assumption costs thousands when families file separate civil suits regardless of criminal outcomes.

Civil courts use different standards of proof than criminal courts. You can win your criminal case but still lose a civil lawsuit and face massive financial damages. This dual threat makes comprehensive coverage essential for serious carriers.

Coverage Exclusions That Void Protection

Every CCW insurance policy excludes certain situations that void your coverage entirely. Most policies exclude incidents that involve alcohol consumption, crimes committed in gun-free zones, or negligent discharges. USCCA terminates coverage if you face conviction of any crime related to the incident.

Some providers exclude domestic violence situations or incidents that involve family members. Right to Bear excludes coverage for incidents that occur during the commission of any crime, even minor infractions like speeding. Second Call Defense recently expanded coverage but still excludes intentional criminal acts and incidents under the influence of drugs or alcohol.

These exclusions highlight why understanding your policy details matters before you need coverage. The next factor to consider involves the actual financial impact these legal battles create.

Analyzing the Real Costs of Self-Defense Incidents

The National Association of Criminal Defense Lawyers promotes the elimination of criminal case fees, but legal expenses in self-defense cases remain substantial. High-profile self-defense cases like George Zimmerman’s 2012 trial exceeded $2.5 million in total expenses. The Crime Prevention Research Center found that justified self-defense incidents still face civil litigation, which creates a double financial threat that destroys families financially.

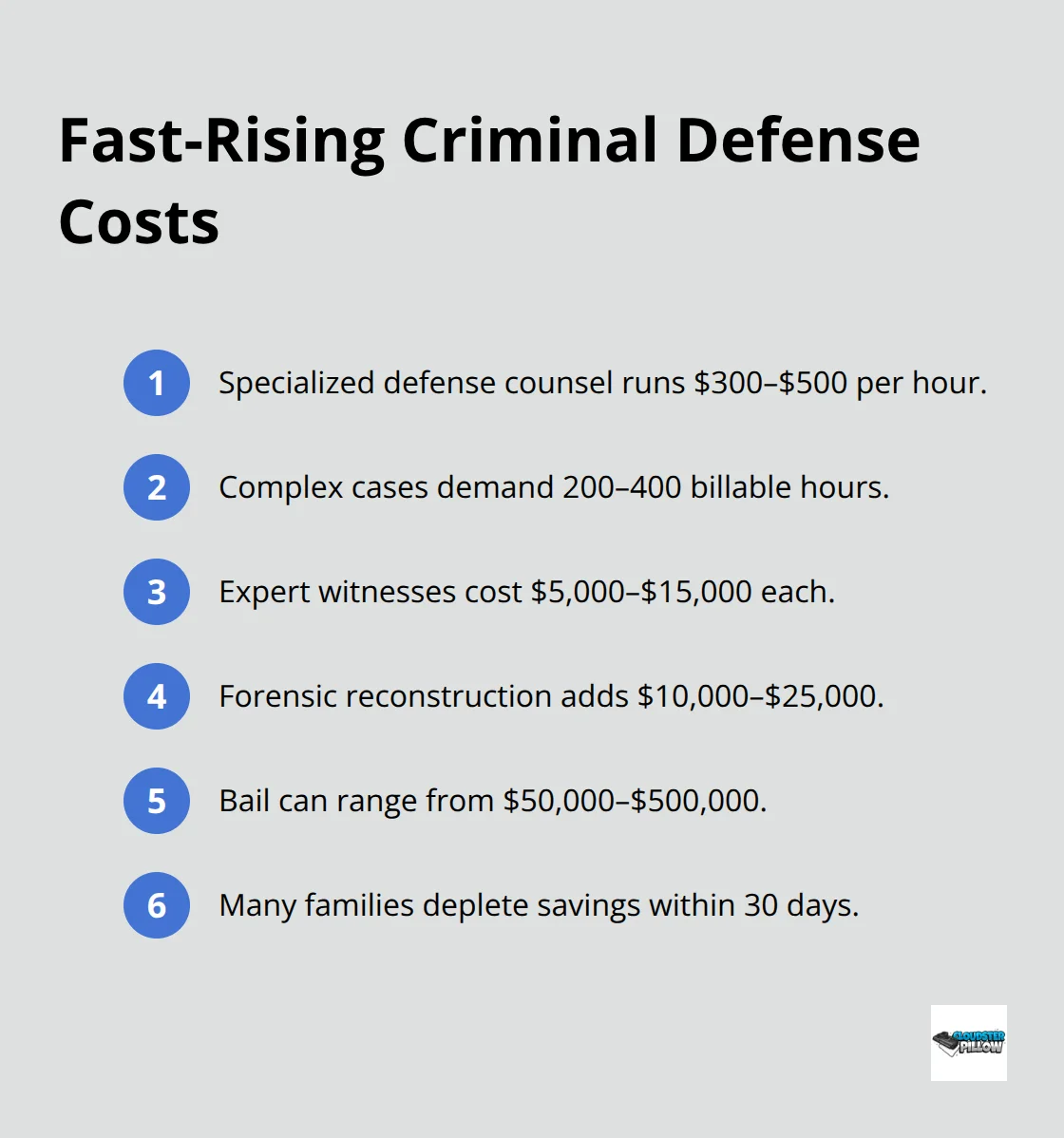

Criminal Defense Expenses Hit Fast and Hard

Criminal cases require immediate action when prosecutors file charges. Defense attorneys who specialize in self-defense law charge $300 to $500 per hour, with complex cases that require 200 to 400 hours of legal work. Expert witness fees add $5,000 to $15,000 per specialist, while forensic reconstruction costs another $10,000 to $25,000. Bail bonds can reach $50,000 to $500,000 (based on the charges filed).

Most families exhaust their savings within the first 30 days of legal proceedings.

Civil Lawsuits Create Long-Term Financial Devastation

Civil cases operate under different rules and often result in massive monetary judgments. Wrongful death cases average $2.8 million in jury verdicts, while injury cases average $200,000 to $800,000 in damages. These cases drag on for 18 to 36 months and generate attorney fees that compound monthly. Medical bills, lost wages, and pain calculations create astronomical damage awards that follow you for decades through wage garnishments and asset seizures.

Hidden Costs Multiply Your Financial Burden

Legal battles generate expenses beyond attorney fees that insurance rarely covers completely. Psychological counseling costs $150 to $300 per session, with trauma cases that require months of treatment. Lost wages during court proceedings average $50,000 to $100,000 for professionals. Private investigators charge $75 to $150 per hour for case preparation (which adds up quickly during complex investigations). Many defendants relocate due to media attention or threats, which adds relocation costs and temporary housing expenses.

These financial realities make the decision about CCW insurance more complex than simple monthly premium calculations. Your personal situation and state laws play major roles in determining whether coverage makes financial sense.

Factors That Determine If You Need Coverage

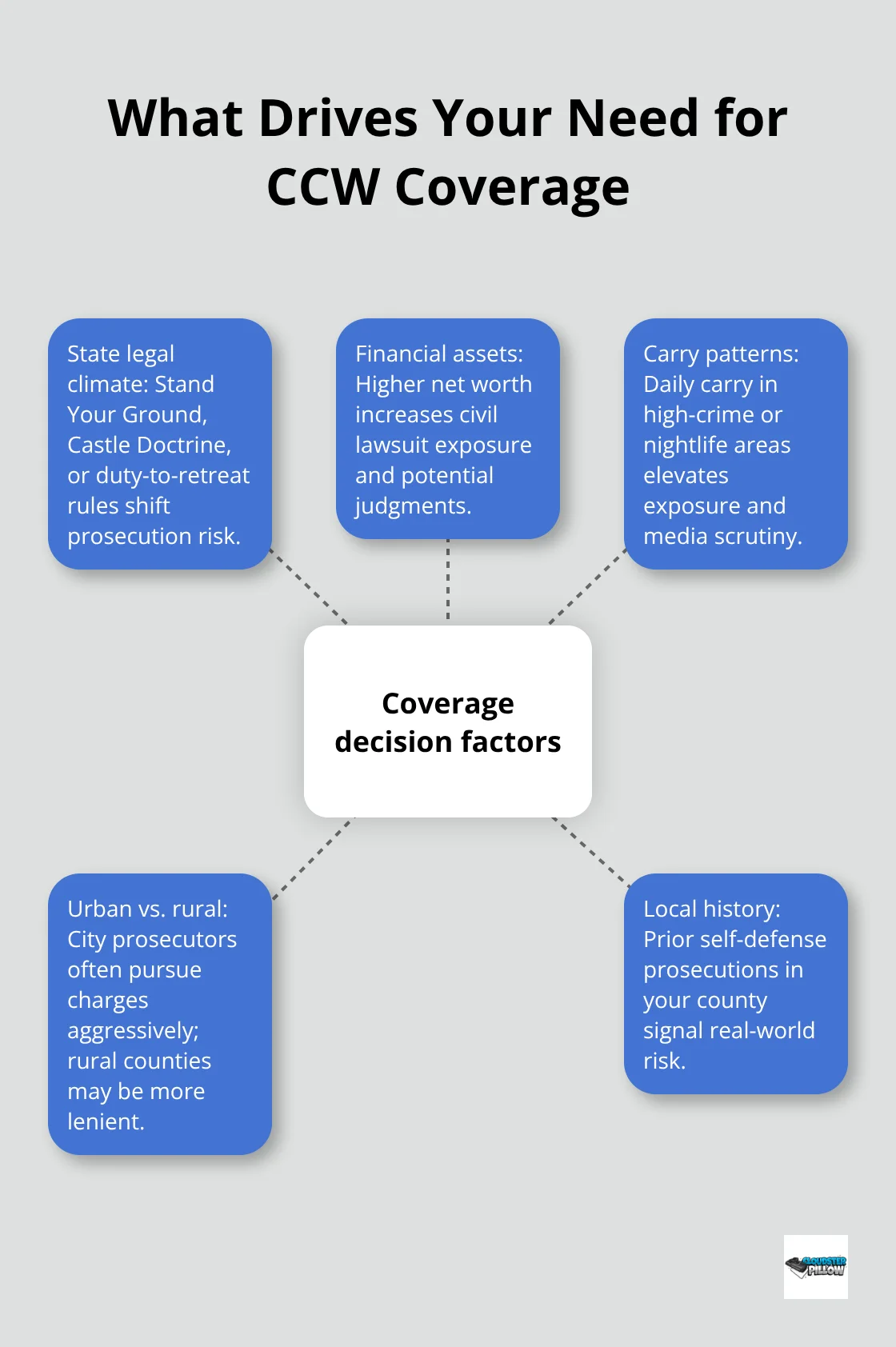

Your state’s legal climate creates the foundation for your coverage decision. States like Texas and Florida have strong Castle Doctrine and Stand Your Ground laws that protect defenders from prosecution, while states like New York and California maintain duty-to-retreat requirements that increase prosecution risks. Research shows that justified self-defense incidents still face significant legal challenges regardless of state protections. Anti-gun prosecutors in major cities like Chicago, Los Angeles, and New York pursue charges even in clear self-defense cases, which makes coverage essential for urban carriers.

State Laws Shape Your Legal Risk

States with constitutional carry laws generally provide stronger legal protections, but civil lawsuits remain a threat everywhere. George Zimmerman faced $2.5 million in legal costs despite Florida’s Stand Your Ground protections. States like Illinois require FOID cards and create additional legal complexities that increase defense costs.

Rural counties typically have gun-friendly prosecutors who rarely charge defenders, while urban jurisdictions aggressively prosecute gun owners. Check your county’s prosecution history for self-defense cases to gauge real-world risks.

Financial Assets Determine Coverage Priority

High-net-worth individuals face greater civil lawsuit exposure because plaintiffs target defendants with substantial assets. Homeowners with significant equity, business owners, and professionals with high incomes become prime targets for wrongful death and injury claims. Wrongful death settlements average nearly $1 million, which makes unlimited civil liability coverage non-negotiable for wealthy carriers. Lower-income carriers might prioritize criminal defense coverage since criminal convictions destroy employment prospects and create long-term financial devastation.

Carry Patterns Multiply Your Exposure

Daily carriers who frequent high-crime areas face exponentially higher risks than occasional carriers in safe neighborhoods. Urban carriers encounter more potential threats but also face hostile legal environments that prosecute defenders aggressively. Carriers who frequent bars, nightlife districts, or politically sensitive locations increase their legal exposure significantly since alcohol-related incidents and politically charged locations generate media attention and prosecutorial pressure. Professional drivers, security personnel, and business owners who carry cash face elevated risks that justify comprehensive coverage regardless of personal wealth levels (especially in major metropolitan areas).

Final Thoughts

CCW insurance costs $150 to $600 annually, while legal defense expenses average $500,000 per incident. The math favors coverage for most carriers, especially those with assets worth protection or who carry in high-risk environments. Your decision depends on three factors: state legal climate, personal financial situation, and carry frequency.

Urban carriers in anti-gun jurisdictions face the highest prosecution risks, which makes unlimited coverage essential. Rural carriers in gun-friendly states might prioritize criminal defense over civil liability protection. A $30 monthly payment protects against bankruptcy from legal fees that destroy families financially (while high-net-worth individuals need comprehensive civil liability coverage).

Prosecutors increasingly target gun owners regardless of justification, and civil attorneys pursue deep-pocket defendants aggressively. Your financial future depends on preparation before incidents occur. Comfortable carry builds confidence for daily preparedness, and we at Cloudster Pillow designed our holster wedge to enhance concealment and comfort for AIWB and IWB holsters, which helps carriers maintain consistent readiness while they protect their financial security through smart insurance decisions.